A support ticket in the insurance sector costs between 8 and 22 euros on average. The same answer delivered by an AI agent grounded in your data: less than 0.08 euros. The question is no longer “should we automate?” but “why did we wait so long?”. In this article, we will see why the future of the policyholder relationship is no longer tied to the support desk alone.

Work organisation and efficiency

A typical day for a customer service advisor

Ask any customer service manager at an insurance company: what share of your incoming volume truly requires the expertise of a trained advisor?

The honest answer hovers around 30 to 35%.

The rest, that is 65 to 70% of interactions, concerns repetitive factual questions: the status of a claim, the amount of a deductible, a document to provide, a reimbursement deadline, a certificate to reissue.

Moreover, these are tasks that your advisors handle in 30 seconds, yet they consume the majority of their available time (Accenture Insurance Technology Vision 2024). Imagine how your productivity would look if you gave that time back to your teams?

This imbalance is not a recruitment issue. It is an architecture issue.

The cost of a so-called “level 1” ticket

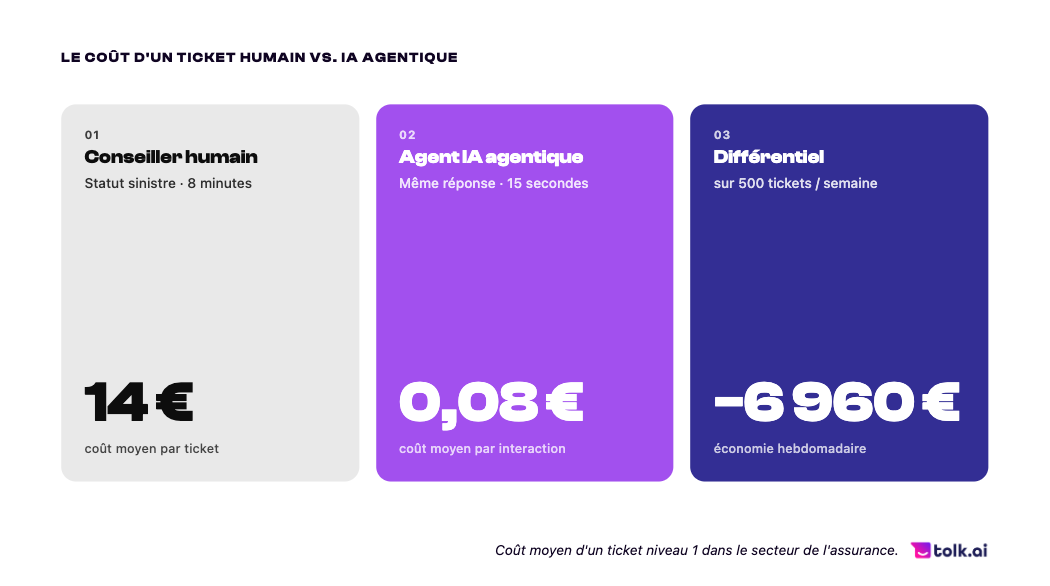

For example, take the simplest claim in your portfolio: a broken windscreen.

The policyholder calls for a follow-up three days after filing the claim. The advisor has to log into your CRM, open the claims management tool, reconstruct the timeline of the file, check whether a document is missing, and formulate a clear answer.

A few calculations: actual interaction time: 7 to 9 minutes. Average cost: 14 to 18 euros.

The same information, accessible through an AI agent connected to your CRM and your claims tool, would take 15 seconds. Its cost? Less than 0.10 euros.

Multiply that by the volume of claim follow-up calls per week. The cost line appears clearly in your reporting, it is simply not labelled as such.

Ultimately, the main challenge is to automate in order to free up time and optimise your costs. We offer you 3 concrete cases where automation has a crucial impact.

Three areas where automation changes performance

1. Document requests

Annual premium statements, proof of coverage, reimbursement tables: these requests represent up to 30% of incoming enquiries in policyholder relationship departments (France Assureurs, digital barometer 2024). Each one ties up an agent for a task that is entirely automatable, with no human added value.

2. Coverage questions outside business hours

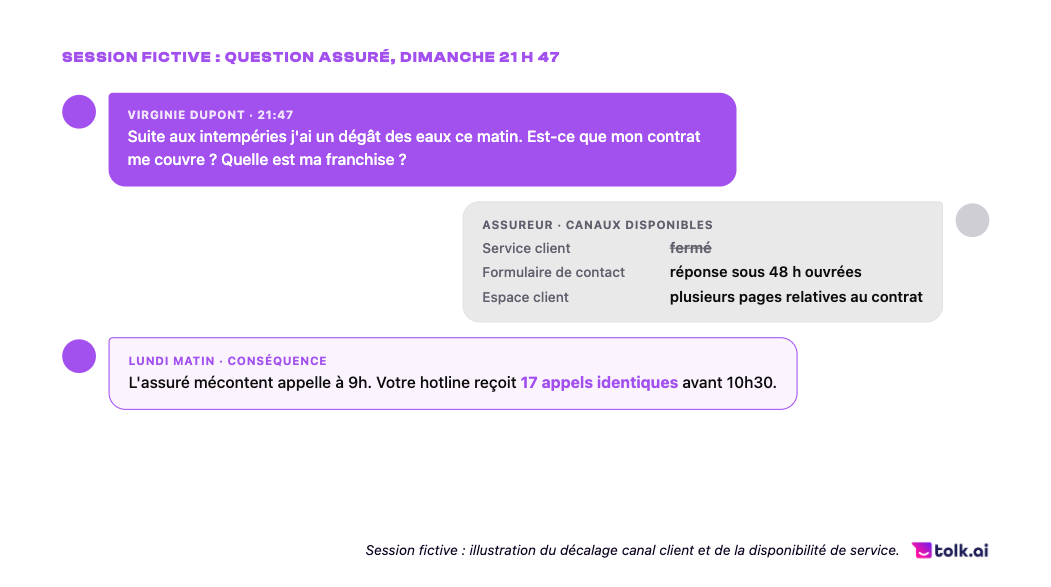

A policyholder who discovers water damage on a Sunday evening cannot reach their advisor. They look online for an answer in their specific terms, fail to find it, and call back on Monday morning. Your hotline absorbs a predictable and entirely avoidable surge in load. 78% of policyholders prefer to resolve their request outside business hours when they have the option (Ipsos, 2024).

3. Coverage checks before purchase

A prospect hesitates between two levels of coverage. They send an email at 7pm. They receive an answer the next day at 10am, having meanwhile signed up with a competitor who replied within minutes through its AI agent. This ticket appears in no performance report. It is invisible, just like the lead it represented.

Chatbot or AI agent: what are the differences?

First, it is important to keep in mind that a first-generation chatbot answers. Unlike an agentic AI agent, which answers and acts.

When it comes to agentic AI, the agent can also send the requested document directly within the conversation, create a preliminary claim file, trigger a priority callback for a complex case, update a postal address, check in real time the reimbursement balance available on a health contract, and so on. The possible use cases are countless!

Moreover, it carries out these tasks with no ticket opened, no delay and no human intervention for standard cases.

This distinction is the key to the results observed in the most advanced deployments:

- -50% processing time on simple claims,

- +25% qualified leads on subscription journeys with an AI agent available 24/7 on a website,

- -60% tickets on automatable document requests,

- Availability 24/7, with no additional payroll cost.

Your advisors are trained to advise, not to do document research

Ultimately, transforming the policyholder relationship does not require more advisors. It requires a precise rebalancing between the capabilities of AI and human values.

The companies that achieve this rebalancing in 2026 will not only cut their costs. They will free their experts for the moments that carry real added value: wealth advisory, the handling of complex claims, and retention on high-stakes portfolios. Furthermore, the insurers who take this turn provide differentiating support to their policyholders, because the experts have the time to assist the profiles that need it most.

In our next article, we will see why the technical architecture of your AI determines your regulatory exposure, and how sovereign hosting has become a prerequisite, not merely a technical or regulatory constraint.

In the previous article, we discussed the legal risk linked to the hallucinations of conventional AI and the possible solutions.