Why entrust your policyholder relationship to an AI that does not know your contracts? That means exposing your company to a risk your legal department has not yet quantified. In this article we will discuss the risks linked to generic AI in insurance: context, definition and advice for anticipating the impacts.

The illusion of the “ready-to-use” chatbot

Since 2023, the general management of insurance companies have all received the same pitch: “Deploy a GPT chatbot, cut your support costs by 40%.” The message is appealing. And yet, legal departments are sounding the alarm.

Because there is a reality that mainstream AI vendors carefully gloss over: a generic AI does not know your contracts. It is unaware of your coverage tables, your exclusion clauses, and your in-house underwriting rules. And in the insurance sector, an approximate answer is not a clumsy slip, it is professional misconduct.

Generic AI in insurance represents an invisible risk

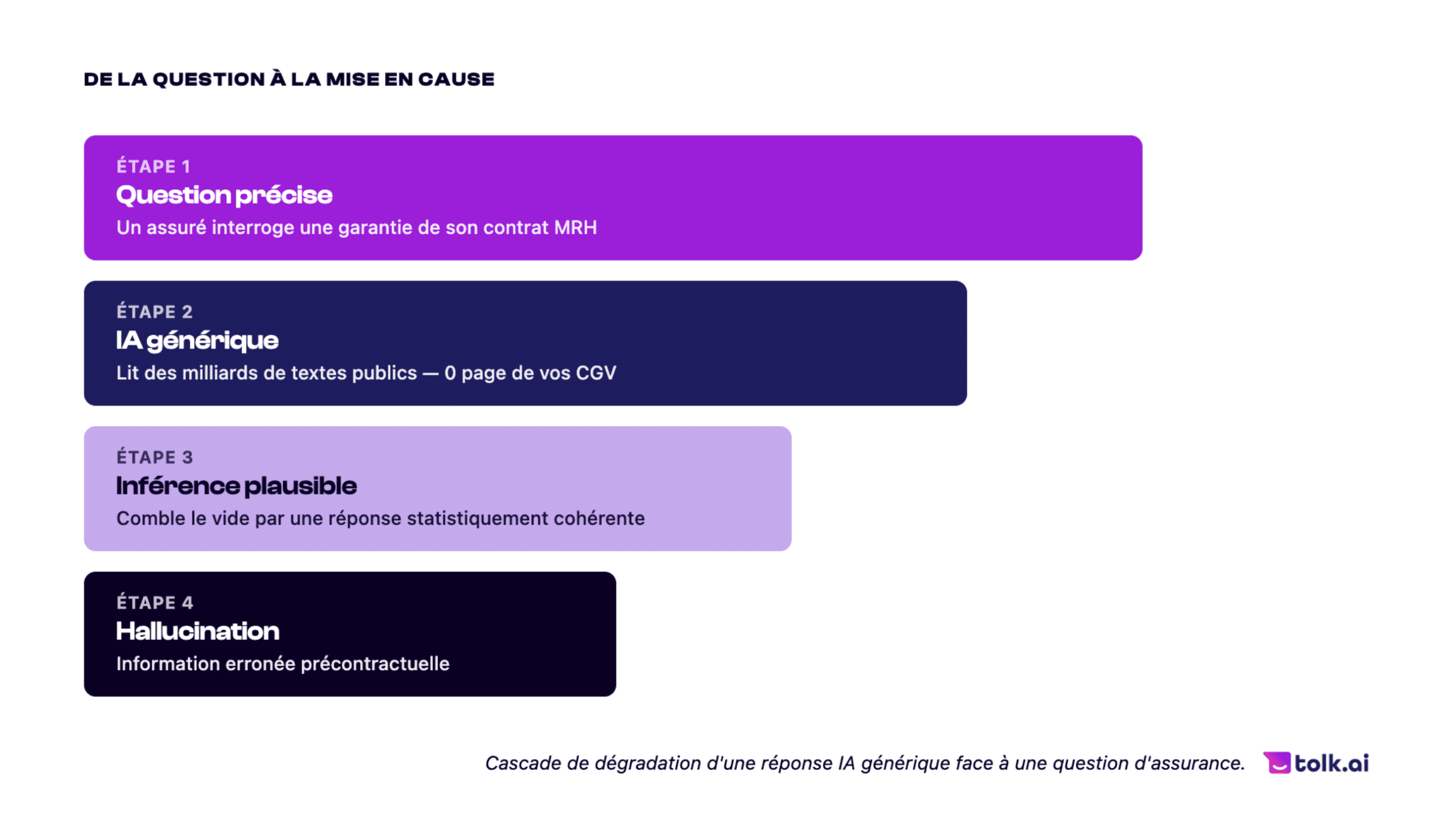

Generic LLMs are trained on billions of public texts. They are able to produce fluent and plausible answers. But faced with a policyholder’s precise question, they fill their gaps by inference. They “hallucinate”, and in insurance, a hallucination has a legal name: incorrect pre-contractual information.

This risk funnel does not appear in any standard report. Yet this is where your next liability claims will be decided.

1. An uncomfortable figure: 3 scenarios with direct exposure

Scenario A: The incorrect advice on a coverage.

A policyholder asks whether their home insurance contract covers the thawing of pipes. The AI answers positively, based on generic market wording. This specific contract excludes that claim in a barely visible clause. The policyholder does not file urgently. The damage worsens.

In your dashboard: session resolved, ticket closed, 0 escalation. Reality: a liability claim for incorrect information.

Scenario B: The unvalidated commitment.

A prospect asks the chatbot about a coverage extension. The AI confirms a coverage that is absent from the standard offer. They sign. When the claim arises, the refusal to cover generates a formal complaint. Under the IDD, responsibility for pre-contractual information lies with the company, not with the technology provider.

Scenario C: The data leak.

Most mainstream LLMs are hosted in the United States and subject to the Cloud Act. Your health, wealth and claims data (all classified as sensitive by the RGPD) transit through servers outside European sovereignty.

2. The diagnosis: why your current tools expose you

If you already have a chatbot or a FAQ, you think you are covered. It is often the opposite.

The generic AI chatbot does not know your terms and conditions. It does not know your specific terms or your endorsements. If it does not know, it does not say “I do not know”, it answers anyway with a statistical confidence that your policyholder will interpret as a contractual guarantee.

The static FAQ, for its part, asks the policyholder to leave their funnel to read 2,000 words. No one wants to search for information: everyone wants to receive an answer.

3. The regulatory framework that changes the game

Three texts create direct obligations on the quality of the information delivered, including by your AI systems:

- The IDD (2016/97/EU) requires that all pre-contractual information be clear, accurate and not misleading. Automated channels are not exempt.

- The ACPR published its first guidelines on AI in financial services in 2023: traceability of automated decisions and audit capability foremost.

- The AI Act classifies AI systems used to advise on insurance in the high risk category: documentation, transparency and human oversight are mandatory. Discover our article on the subject.

These texts are not theoretical. The first sanctions are emerging at the European level. This topic is no longer an IT department concern, it is a key strategic issue.

4. The business impact: precision as a competitive advantage

Furthermore, insurers that integrate AI rigorously record measurable gains. The difference does not come from the LLM model chosen, it comes from the architecture.

High-performing solutions ground the LLM strictly in your document corpus through a technique called RAG (Retrieval-Augmented Generation). The AI can only answer from what you have provided it. It cites its sources. If it does not know, it says so.

- 80% of level 1 questions automated and handled without human intervention,

- Every interaction traced and auditable to meet ACPR requirements,

- Data on sovereign infrastructure, out of reach of the Cloud Act,

- +25% qualified leads on subscription journeys with a contextual agent (insurance AI sector benchmarks 2025).

Managing the risk linked to generic AI in insurance

In conclusion, the risk of generic AI in insurance is not a technological risk, it is a legal and reputational risk that your compliance committee has not yet included in its mapping.

Finally, the companies that deploy an AI grounded in their business data in 2026 will not only have reduced their support costs. They will have turned their policyholder relationship into a defensible competitive advantage.

In our next article, we will explore how to move from processing information to automated execution: why the future of the policyholder relationship no longer lies solely in resolving support tickets.