ACPR compliance, data sovereignty, traceability, AI Act: an AI project in insurance engages your regulatory responsibility well before going into production. Here is the validation protocol that legal and compliance teams must run upfront.

First, AI projects in insurance do not fail on technology. They fail on governance. Often, a deployment validated technically can find itself blocked six months later by the legal department over a point that had not been anticipated. These elements are not mere details. Thus, they determine whether your project is legally deployable or not.

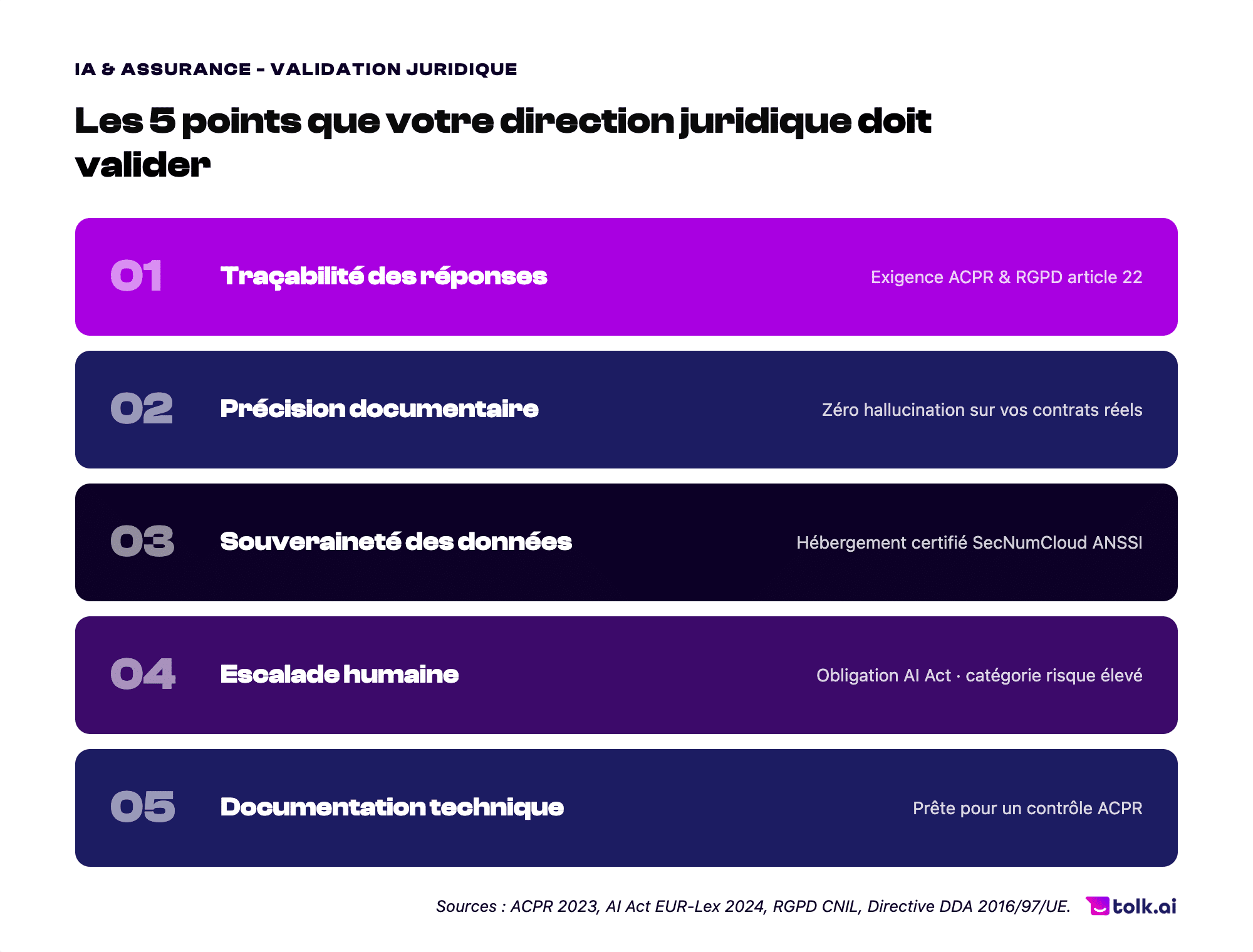

Here are the 5 questions your legal and compliance teams must ask. We will also see how a one-hour session with an AI expert on your real documents makes it possible to answer them.

Step 1: validate the traceability of the answers produced by the AI

First, the Autorité de contrôle prudentiel et de résolution (ACPR, the French prudential supervisory and resolution authority) and the General Data Protection Regulation (GDPR) require that any automated decision be traceable and explainable. In practice, each answer produced by the system must be able to be audited. For example, which documentary source was used, which precise clause, at what moment.

Without complete logging of interactions, you can neither defend your position in the event of a dispute nor demonstrate your compliance during a regulatory inspection. This point cannot be assessed on a generic demonstration. It is validated on your own contracts, by observing live what the system produces and how it justifies it.

Consequently, the question to ask concerns the tracking of the AI interactions, with the documentary sources mobilized for each answer.

Step 2: test accuracy on your most demanding documents

Secondly, the Insurance Distribution Directive (IDD) requires that the information provided to policyholders be accurate and verifiable. A generative artificial intelligence system not anchored on your internal documents can produce incorrect answers about guarantees, deadlines or exclusion conditions, with a confidence of tone that makes the error undetectable for the policyholder.

The Retrieval-Augmented Generation (RAG) architecture solves this problem by constraining the system to answer exclusively from your sources. If the answer is not in the knowledge base, the agent is honest and says so. However, this property must be verified on your real documents: general terms and conditions with cross-references between clauses, amendments that retroactively modify certain guarantees, compensation scales with nested thresholds.

The question to anticipate: what happens when a policyholder asks a question whose answer is not in the connected documentary base?

Step 3: verify data sovereignty

Third, the data processed in insurance is sensitive by nature: health data, asset information, claims declarations. Hosting subject to the US Cloud Act exposes this data to a foreign jurisdiction, regardless of the contracts signed with the provider.

Digital sovereignty is not a sales argument. Thus, it is a compliance requirement for regulated players. Hosting on an infrastructure certified SecNumCloud by the ANSSI (the French national cybersecurity agency) guarantees that your data remains under French and European jurisdiction (without exposure to US extraterritorial law).

The questions to ask: on which infrastructure is your solution hosted? Is it subject to any non-European jurisdiction?

Step 4: configure and document the escalation mechanisms

Next, the European regulation on artificial intelligence (AI Act) classifies AI systems in insurance in the high-risk category. This classification imposes several things:

- effective human oversight,

- documented escalation mechanisms,

- the possibility of manual intervention at any time.

Moreover, an AI agent that does not transfer to a human agent in a traceable way is not deployable within this regulatory framework. Indeed, the escalation thresholds must be defined by your business teams, configured in the AI agent, and verifiable during an audit. During a test workshop, these thresholds can be activated live on your real use cases.

The question to ask: on what criteria does your system decide to escalate, and how is this transfer documented?

Step 5: be compliant with the AI Act

Finally, the AI Act imposes a complete technical specification for high-risk organizations:

- a description of the system,

- the data processing architecture,

- measured performance,

- known limitations,

- incident management procedures.

If your provider cannot supply you with this documentation, you will not be able to respond to a request from the ACPR or the Commission nationale de l’informatique et des libertés (CNIL, the French data protection authority) within the required timeframe.

Furthermore, it is essential to measure these elements before deployment, not after. This is a guarantee of transparency and trust in a commercial relationship with your solution publisher.

AI in insurance: test with no commitment

Our complete solution Genii meets these five requirements natively: complete logging of interactions, RAG anchoring on your documentary bases, Outscale France hosting certified SecNumCloud, configurable and traceable escalation, compliant technical information.

Also, we offer a free 14-day trial to let you measure the effectiveness of our solution Genii. This test is carried out in real conditions with your own use cases, no commitment is required.